Open Enrollment for 2024 Has Begun!

Plans can be as low as $0 month with lower copays and deductibles.

Price:$

Popularity:★★★★

More Infomation

Price:$$

Popularity:★★★★★

More Infomation

Price:$$$

Popularity:★

More Infomation

Price:$$$$

Popularity:★★

More Infomation

Price:$

Popularity:★★★★★

More Infomation

Price:$

Popularity:★★★

More Infomation

The 2024 Open Enrollment for individual and family health insurance will start on November 1, 2023. Existing Covered California policyholders can choose plans with most suitable benefits and premiums for 2024 through consultation and price comparison, and decide whether to adjust their insurance. In 2024, there will still be many insurance companies and plans. People who qualify for premium subsidies may even get a great plan with $0 premium and $0 deductible. For people who currently do not have health insurance and are in the transition period of visa or immigration status, Open Enrollment is also an opportunity for insurance that cannot miss.

- Free annual health check-up

- Primary care visit: $60*

- Specialist visit: $95*

- Laboratory tests: $40

- Outpatient surgery/inpatient hospitalization: full cost until deductible is met, 40% of remaining cost after deductible is met.

- Individual annual out-of-pocket maximum: $9,100

- Click here for more details about the Bronze plan

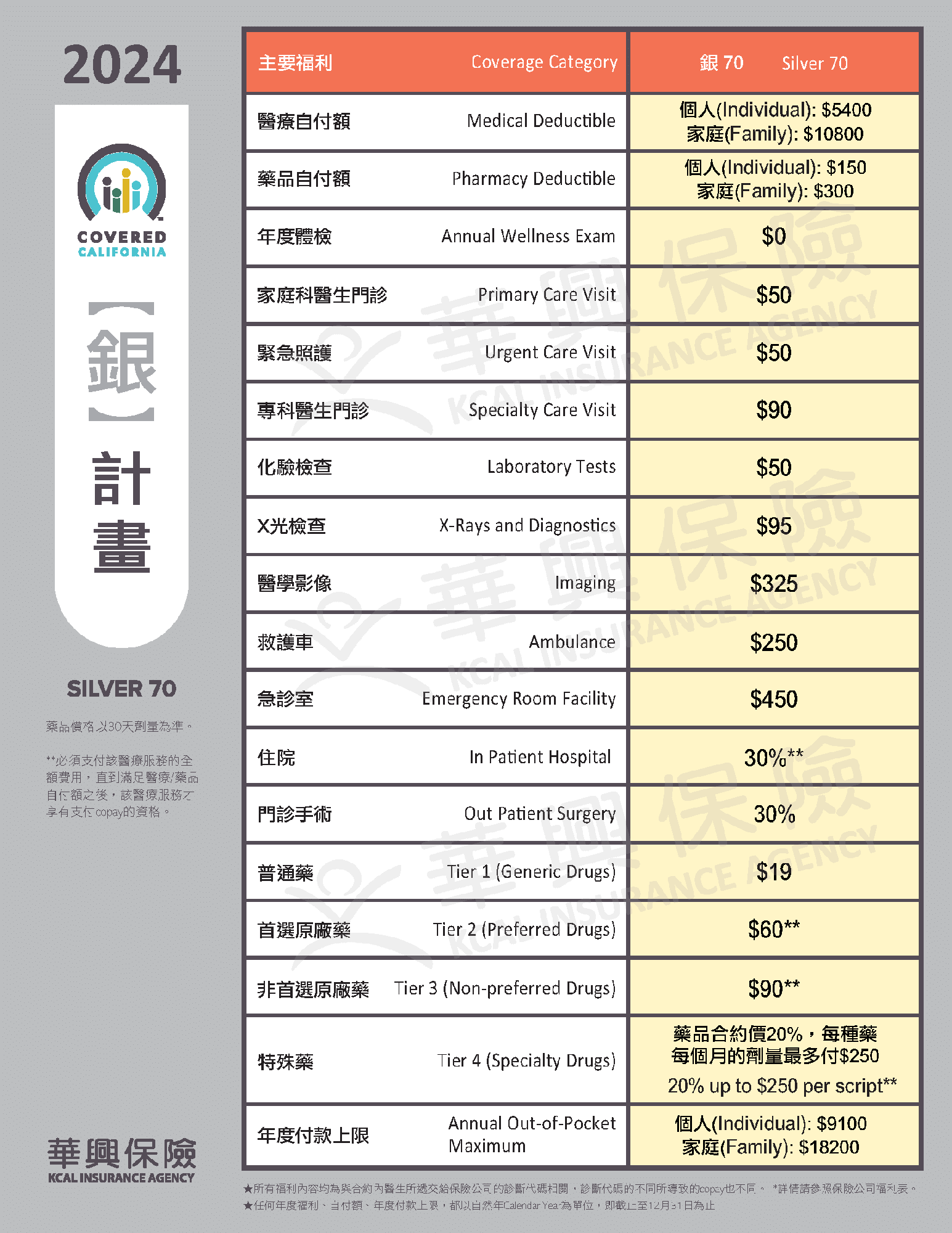

This plan is a balance of premium and benefits with affordable deductibles, outpatient fees and co-pays. The insurance company will cover 70% of the medical expenses, and the insured pays the remaining 30%.

- Free annual health check-up

- Primary care visit: $50

- Specialist visit: $95

- Laboratory tests: $50

- Inpatient hospitalization: 30% of remaining cost after deductible is met

- Outpatient surgery: 30% of total cost

- Individual annual out-of-pocket maximum: $9,100

- Click here for more details about the Silver plan

{kind=link}

This plan works better for individuals and families who frequently need medical treatment. Insured has a lower out-of-pocket payment but the premium is higher. Insurance companies will cover 70%-75% of the medical expenses, and the insured pays the remaining 25%-30%.

- Free annual health check-up

- Primary care visit: $35

- Specialist visit: $65

- Laboratory tests: $40

- Outpatient surgery: $130 per surgery (HMO) or 30% of total cost (PPO)

- Inpatient hospitalization: $330 per day (HMO) or 30% of total cost (PPO)

- Individual annual out-of-pocket maximum $8,700

- Click here for more details about the Gold plan

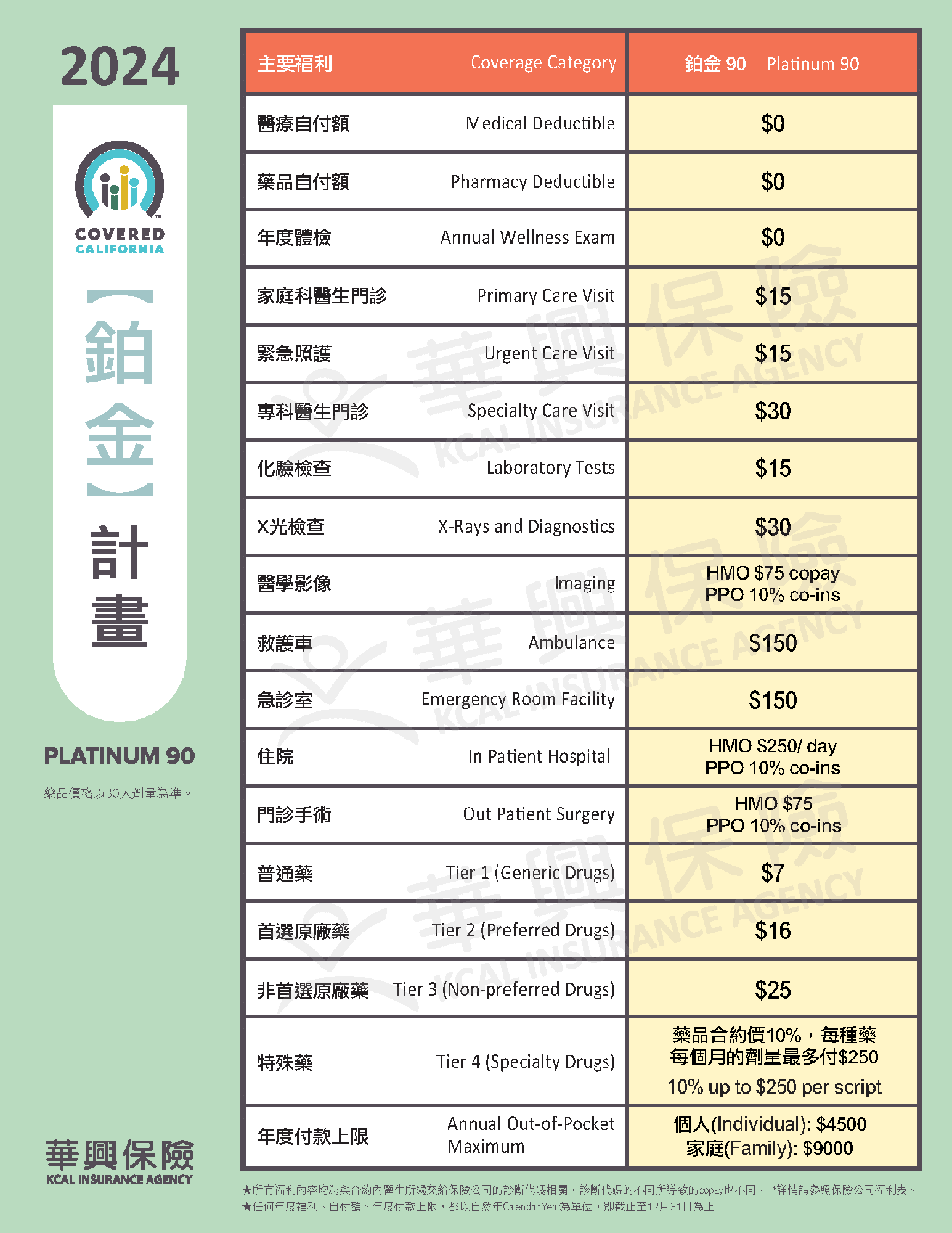

With the lowest out-of-pocket payment cap, this plan is suitable for individuals and families who require frequent medical service and treatment. Insurance companies will cover 90% of medical expenses, and the insured pays the remaining 10%.

- Free annual health check-up

- Primary care visit: $15

- Specialist visit: $30

- Laboratory tests: $15

- Outpatient surgery: $75 per surgery (HMO) or 10% of total cost (PPO)

- Inpatient hospitalization: $225 per day (HMO) or 10% of total cost (PPO)

- Individual annual out-of-pocket maximum: $4,500

- Click here for more details about the Platinum plan

{kind=link}

Affordable health insurance costs with comprehensive protection against serious illnesses. This plan works better for people with good health conditions.

- Free annual health check-up

- Can be combine with HSA and save more taxes

- Insurance will cover all necessary services after the annual out-of-pocket maximum is met

- Individual annual out-of-pocket maximum: $7,050

- Family annual out-of-pocket maximum: $14,100

- Click here for more details about the Bronze HDHP plan

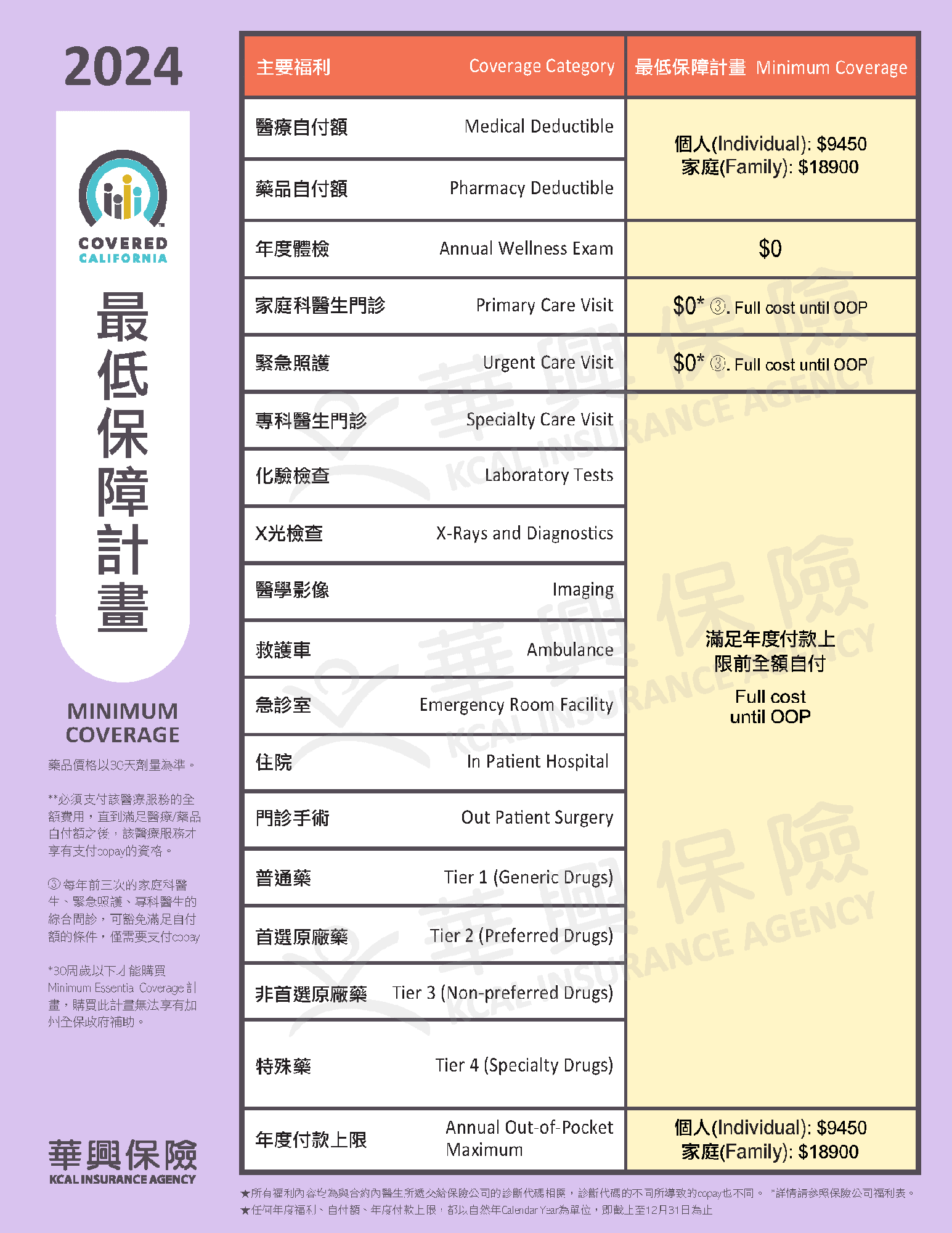

A basic health insurance plan designed for individuals under the age of 30.

- Free annual health check-up

- First three non-preventive visits are free, after the annual out-of-pocket maximum is met, the insurance will cover all necessary services

- Individual annual out-of-pocket maximum: $9,450

- Family annual out-of-pocket maximum: $18,900

- Click here for more details about the minimum coverage plan

{kind=link}

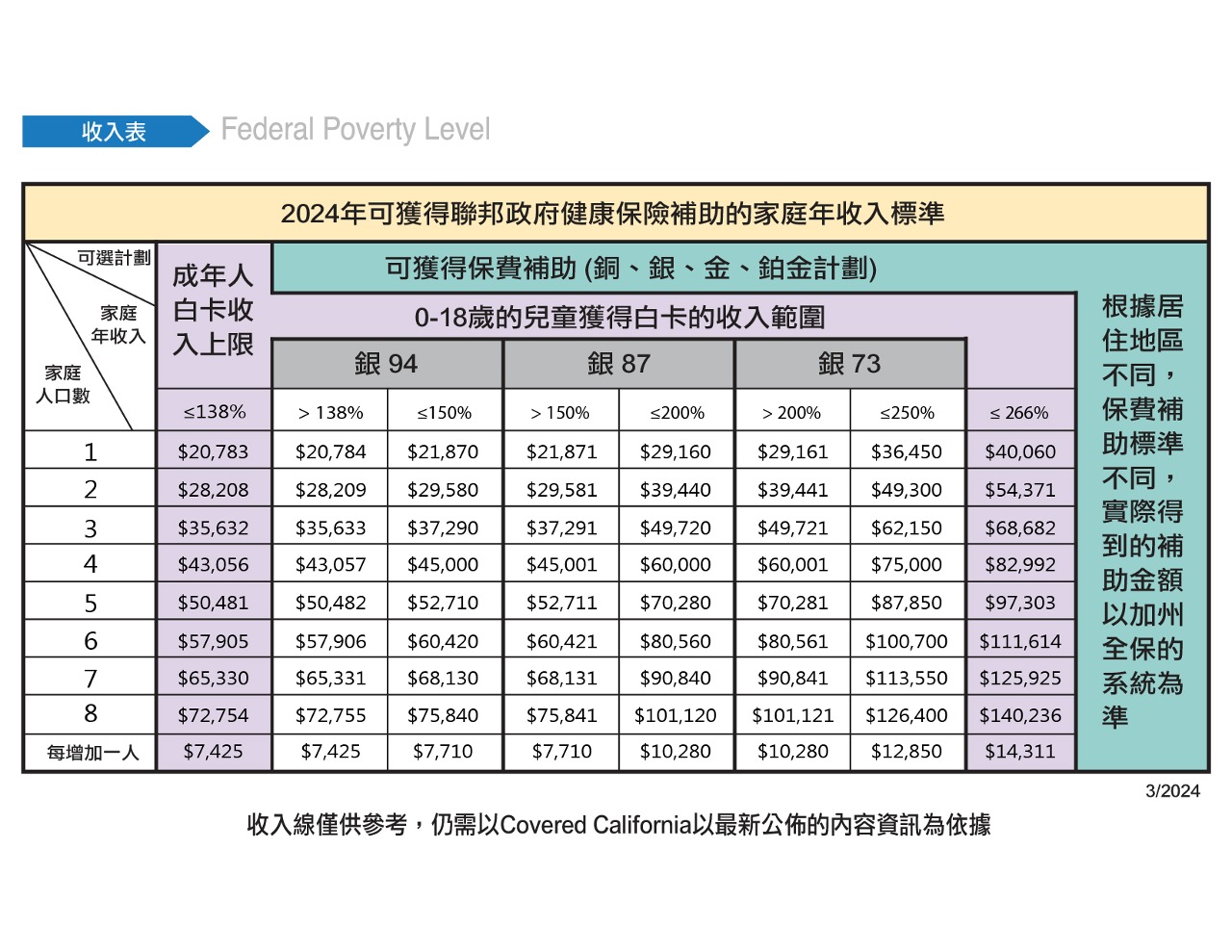

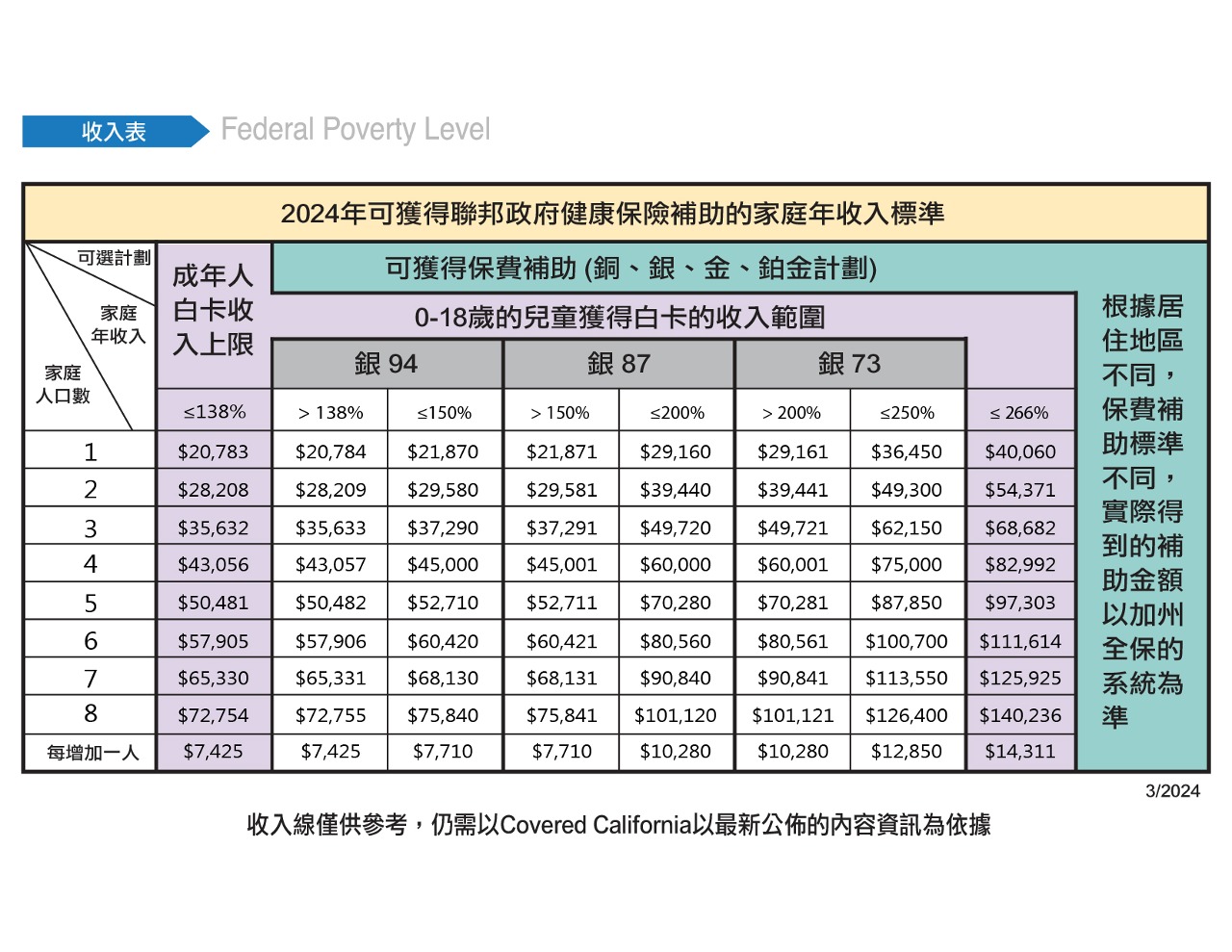

Low Income Individual and Family Insurance Plan Benefits

U.S. citizens or tax residents may qualify for government-subsidized health insurance. Your premiums and subsidy amounts are related to the number of households on the tax return forms and the annual income. You can only enroll during a fixed three-month period each year. Therefore, having a professional, licensed and experienced insurance broker is essential to ensure the best benefits, the lowest Premiums, and the most accurate subsidies and tax credits for you. Families and individuals whose annual income is between 138% and 250% of the federal poverty line have the opportunity to receive affordable plans such as Silver 94, Silver 87, and Silver 73.

| Silver 94 | Silver 87 | Silver 73 | Silver 70 | |

|---|---|---|---|---|

| Primary care visit: | $5 | $15 | $35 | $50 |

| Specialist visit: | $8 | $25 | $85 | $90 |

| Laboratory tests: | $8 | $20 | $50 | $50 |

| Medical & Pharmacy Deductible: | $0 | $0 | $0 | Click here |

| Inpatient Hospitalization: | 10% of total cost | 20% of total cost | 30% of total cost | Click here |

| Outpatient Surgery: | 10% of total cost | 20% of total cost | 30% of total cost | 30% of total cost |

| Individual Annual Out-of-pocket Maximum: | $1,150 | $3,000 | $6,100 | $9,100 |

| Detailed Coverage: | Click here | Click here | Click here | Click here |

| Coverage Explanation: | Listen here | Listen here | Listen here | Listen here |

Health Insurance FAQs

Yes, the penalty for each uninsured resident will be at least $850 per adult and $425 per dependent child under 18 in the household. A family of four that goes uninsured for the whole year would face a penalty of at least $2,550.

If you apply for health insurance through Covered California, you will still have the opportunity to apply and qualify for subsidies.

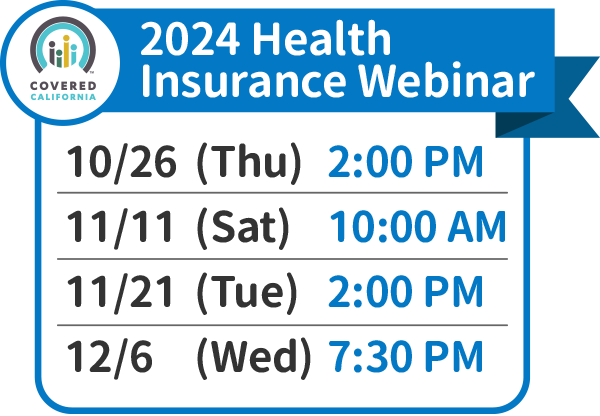

For 2024, Covered California’s Open Enrollment Period is from November 1, 2023 to January 31, 2024.

Individuals could only enroll in health insurance or switch plans during the Open Enrollment Period, which was only a few months of the year. After the enrollment period was over, if they did not qualify for special enrollment, individuals would no longer be able to apply for health insurance or make adjustments to their plans.

In 2024, many insurance companies reduced premiums, government subsidies have also increased significantly, and certain plans offer $0 premiums.

If you are currently using a PPO plan, you might want to consider switching to HMO to save more on premiums. Downgrading your plan is another way to save. If you have a Platinum plan and find it too expensive, you can consider downgrading to the Gold or Silver plans.

You can also open an IRA to reduce the taxable income so that when you apply for government subsidies you will have lower premiums and get better benefits.

For 2024, Covered California’s Open Enrollment Period is from November 1, 2023 to January 31, 2024.

If you are looking for a new plan effective on January 1st, you need to complete the application before December 31st, 2023. If you are looking for a new plan effective on February 1st, you need to complete the application before January 31st, 2024.

For 2024, Covered California’s Open Enrollment Period is from November 1, 2023 to January 31, 2024.

If you miss this open enrollment period, you will not be able to purchase health insurance unless you qualify for special enrollment, in which you would have to apply for health insurance within 60 days of your qualifying life event which include:

1. A child is born, adopted or received into foster care; your child is placed into foster care or is up for adoption

2. Loss of employer-sponsored coverage, or your COBRA coverage is exhausted (Note: Not paying your COBRA premium is not considered loss of coverage)

3. Loss of Medi-Cal coverage

4. Moved to California from out of state or moved within California and gained access to at least one new Covered California health insurance plan

Because you do not have a SSN, you won’t be able to purchase general health insurance used by United States citizens. Basic travel insurance also won’t be able to cover pre-existing conditions such as diabetes, high blood pressure, pregnancy, and more. However, we recommend taking a look at our “MYT” health insurance. (Click here for more information.)

Covered California and the IRS are connected in the sense where Covered California uses the household income and household size on the 1040 tax form to calculate health insurance premiums and check for eligible federal subsidies for the applicant. If you are a resident with a taxable income (citizen, green card holder, working visa holder, etc.), and your family income meets the requirement, you may qualify for subsidies and medical costs.

Based on your annual household income, you may qualify for federal subsidies in the form of Medi-Cal, premium assistance, or cost-sharing reductions. To determine whether you qualify for premium assistance, please refer to this chart.

{kind=link}

To find your adjusted gross income, take a look at Line 2A, 6A and 11 on Form 1040.

If you have your paycheck statement, rental income, interest income, or income from the EDD, you can use it as proof of income. If you do not have any valid documents, you can ask your accountant or employer to provide you with a signed proof of income statement.

If you have non-taxable social security benefit, income living abroad or non-exempt interest, you should include these as income to calculate the accurate MAGI amount.

*Please consult your CPA for further tax questions.

If you want to enroll for health insurance with subsidies during open enrollment, you cannot cancel your Medi-Cal coverage.

If you do not need subsidies, you can cancel your Medi-Cal coverage and purchase health insurance without subsidies during open enrollment.

You will need to provide proof of income to the county office where you reside to cancel your Medi-Cal coverage before you can apply for general health insurance.

After President Biden signed the American Rescue Plan, California’s health insurance market will face three major changes. First, those who received extra premium subsidies due to a lower reported income will not need to return it when filing taxes for 2020 if their actual reported income is higher. Secondly, those insured with Covered California will automatically have their premiums recalculated and receive more premium assistance. Lastly, middle-to-high-income individuals who were not eligible to apply for premium subsidies in the past may now become eligible to apply for premium subsidies.

PPO premiums continue to increase as it has done so in the past few years. If your health is in good condition and you do not expect to go to the doctor’s often, then you can consider switching to an HMO or EPO plan.

You can also open an IRA to reduce the taxable income so that when you apply for government subsidies you will have lower premiums and get better benefits.

If your doctor is not contracted with your current insurance company, then you can switch to an insurance company that your doctor is in contract with.

If your primary care physician only accepts group health insurance and you are self-employed, or a 1099 employer, feel free to contact KCAL to see what your options are.

Since the benefits would be the same, one way to help you choose the right insurance company is based on the quality of service and the size of the medical network.

If you want to be able to see a doctor easily and don’t want to delay treatment due to conflicts with your medical network, then Kaiser Permanente would be the best option. Its comprehensive medical system and latest medical equipment make it easy to see a doctor.

If the company you work at offers you and your family group health insurance, you won’t be able to purchase insurance with government subsidies for you and your family. As long as the company-provided health insurance is considered affordable and meets certain standards, then you won’t qualify for subsidies.

If you and your family are applying for subsidies when your company offers group health insurance to you and your family, then your subsidies will be returned to the government.

However, if the out-of-pocket amount you have to pay for the employer-sponsored plan’s premium (not including the premium your family pays) is 9.61% higher than your annual household income, then you and your family can apply for government subsidies for health insurance after submitting necessary documentation.

“COVERED CALIFORNIA,” “CALIFORNIA HEALTH BENEFIT EXCHANGE”, AND THE COVERED CALIFORNIA LOGO ARE REGISTERED TRADEMARKS OR SERVICE MARKS OF COVERED CALIFORNIA, IN THE UNITED STATES.

This website is owned and maintained by KCAL Insurance Agency, which is solely responsible for its content. This site is not maintained by or affiliated with Covered California, and Covered California bears no responsibility for its content. The e-mail addresses and telephone number that appears throughout this site belong to KCAL Insurance Agency and cannot be used to contact Covered California.