Help Center

Health Insurance FAQs

Is it required to buy health insurance? Is there a penalty if I don't purchase health insurance?

Yes, currently the penalty for not having coverage the entire year will be at least $850 per adult and $425 per dependent child under 18 in the household when you file your state income tax return. A family of four that goes uninsured for the whole year would face a penalty of at least $2,550.

If you apply for health insurance through Covered California, you will still have the opportunity to apply and qualify for subsidies. The Open Enrollment Period for purchasing health insurance in 2023 starts from November 1, 2022 and ends on January 31, 2023. If you would like your policy to become effective on January 1, 2023, then you will need to enroll and submit your application by December 30, 2022.

During this Open Enrollment Period, you can also update or change your health plan if you would like to do so. If you miss this time period, you will not be able to purchase health insurance at any point for the rest of the year, unless you qualify for special enrollment.

What is the penalty if I don’t have health insurance?

Currently the penalty for not having coverage the entire year will be at least $850 per adult and $425 per dependent child under 18 in the household when you file your state income tax return. A family of four that goes uninsured for the whole year would face a penalty of at least $2,550.

Do I qualify for special enrollment?

- Legal separation or divorce

- Marriage or domestic partnership

- Cessation of dependent status (attaining the maximum age to be eligible as a dependent child)

- Birth, adoption, or placement for adoption

- Loss of coverage due to termination of employment or reduction in the number of hours of employment

- Relocating to California

- Returning from military active duty

- Release from incarceration

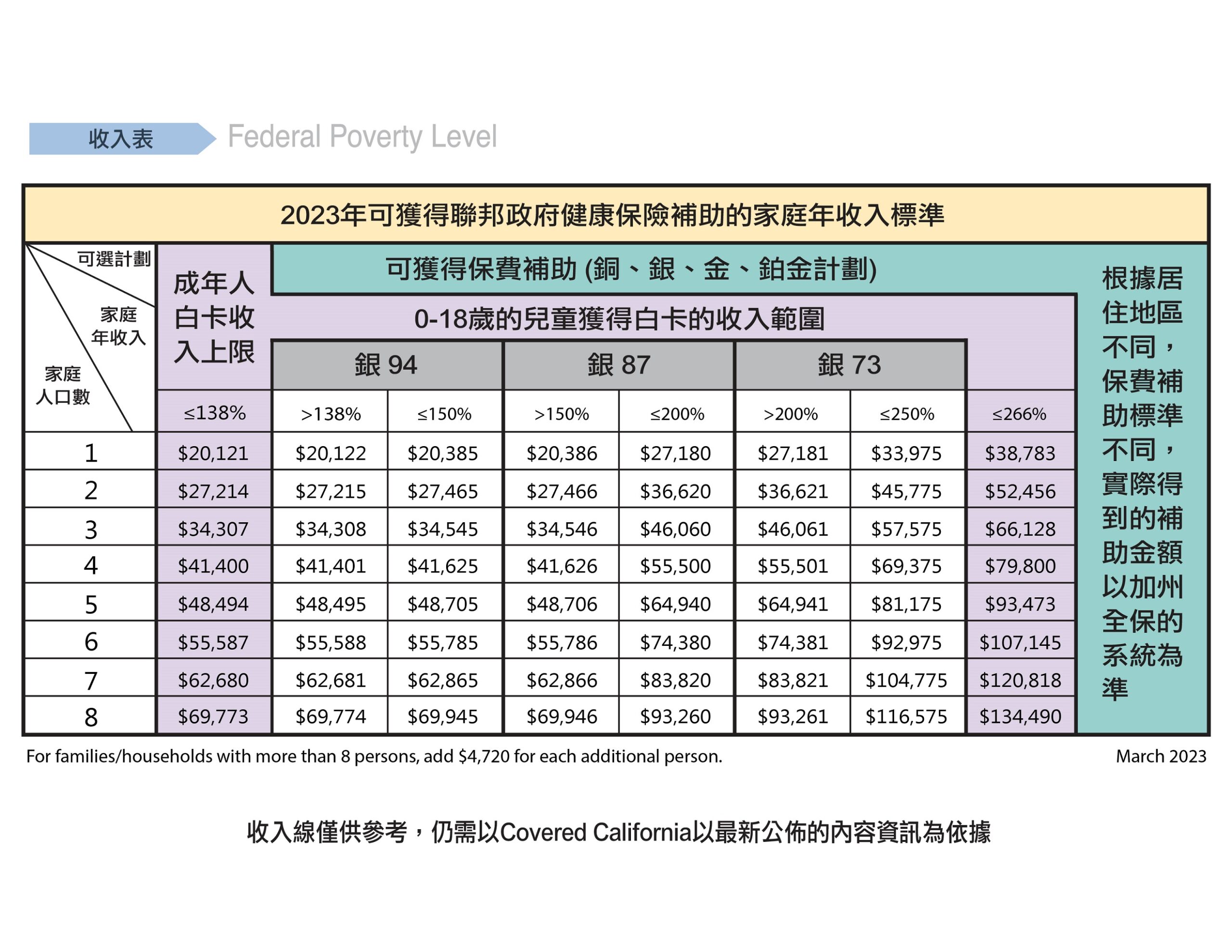

Do I qualify for federal subsidies?

Covered California and the IRS are connected in the sense where Covered California uses the household income and household size on the 1040 tax form to calculate health insurance premiums and check for eligible federal subsidies for the applicant.

Based on your annual household income, you may qualify for federal subsidies in the form of Medi-Cal, premium assistance, or cost-sharing reductions.

As long as you are a resident with a taxable income, you are required to have health insurance whether it’s through your employer, Covered California, etc. If you do not, you will be penalized and fined. To determine whether you qualify for premium assistance, please refer to the chart below:

What are HMO, EPO and PPO?

Here are the main differences among the three plans:

| HMO | EPO | PPO | |

|---|---|---|---|

| Must choose a primary care physician | Y | N | N |

| Referrals are required to see specialists | Y | N | N |

| Benefits outside medical network | N | N | Y |

When choosing a health plan, take into consideration you and your family’s needs. If you have a primary care physician you want to see, make sure your primary care physician is in that network.

Which health insurance plan should I choose?

There are plenty of individual health insurance plans to choose from. Here are the most common types:

HMOs (Health Maintenance Organization). HMOs are one of the most affordable health plans available, and they offer comprehensive coverage. HMOs create networks of doctors, hospitals, clinics, specialists, and other care providers. Most HMO networks consist of thousands of health care professionals, ensuring you’ll have convenient access to medical care when you need it.

PPOs (Preferred Provider Organization). PPOs are affordable individual health insurance plans with an added benefit – you’ll have coverage with any health care provider. That means you can see any doctor or specialist you want, and your plan will cover the care. PPOs are great for flexible, comprehensive, and affordable health care.

Health Savings Account (HSA) Plans. There are 2 parts to HSA coverage: a high-deductible plan and a Health Savings Account. The high-deductible plan provides catastrophic coverage and features low monthly premiums. The HSA is a tax-free savings account where you save money to pay for routine medical expenses.

Fee For Service (FFS) Plans. FFS plan is a traditional form of individual health insurance. You get the care you need and then you’re reimbursed for a percentage of the cost.

What are Obamacare's Essential Health Benefits?

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services, including behavioral health treatment

- Prescription Drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services, including dental and vision care

Related reading: Take Advantage of Obamacare’s 10 Essential Benefits

When can I apply for health insurance?

The 2023 Open Enrollment Period starts on November 1, 2022. Please feel free to contact us at KCAL! We’d be more than happy to help you enroll or switch insurance plans for 2023!

Open enrollment for Covered California health insurance plans happens once a year. During this open enrollment period, individuals can enroll, switch plans, and get subsidies. Unless you meet special conditions, open enrollment is the only time of year you can get a major medical plan that counts as minimum essential coverage in the individual and family market.

Can I apply for healthcare at any time?

Unless you qualify for special enrollment, you can only purchase health insurance during the Open Enrollment Period, which occurs only once a year.

The 2023 Open Enrollment period starts on November 1, 2022 and ends on January 31, 2023. If you’d like your policy to become effective by January 1, 2023, you must apply by December 31, 2022.

How can I apply for health insurance?

- Social Security Number (SSN) of entire household

- Proof of citizenship (U.S. passport) or proof of residence (i.e. green card) for entire household

- 2021 tax forms

- Proof of wages from the past month

If you are already a Covered CA member, please bring the additional documents with you when you come to our office:

- Current health insurance information (insurance card)

- Covered CA renewal notice that you received in the mail (green envelope)

How do I calculate my monthly premium and subsidy amount?

How can I lower my monthly premium?

What will my deductible be?

How can I insure just my child?

However, many health insurance companies require one policy per child. So if you have more than one child, try entering just one child to see a larger selection of plans and prices. Feel free to apply for each child separately.

When should I consider a Health Savings Account (HSA)?

- Not entitled to benefits under Medicare

- Be covered under a high deductible health plan

- May not be covered under any health plan that is not a high deductible health plan

- Not be claimed as a dependent on another person’s tax return

What are the advantages?

- Contributions to the account are tax deductible

- Amounts in an HSA belong to the individual and are fully portable

- Amounts in an HSA earn tax-free interest

- Unused amounts in the account at year-end remain available for future years

- Distributions are not taxed if used for qualifying medical expenses

Who should buy individual health insurance?

- Self-employed.

- People who work for a small business that does not provide a health plan.

- Those who do not obtain individual health insurance.

Can individuals with pre-existing conditions apply for health insurance?

Workers’ Compensation Insurance FAQs

What is Workers' Compensation Insurance?

Employer’s Liability coverage, also included in these policies, protects your company in the event that an employee claims that his or her injury or illness was caused by your company’s negligence or failure to provide a safe workplace.

What are the benefits of Workers' Compensation Insurance?

What does Workers’ Compensation cover?

What are the penalties for not having Workers’ Compensation?

1. The DLSE can issue a stop work order and require employers to cease all business operations at the worksite until they furnish proof of workers’ compensation insurance.

2. Employers are still required to pay salaries until they reopen.

3. The DLSE will assess a penalty of a minimum of $1,500 up to $100,000 per employee.

4. If an employee gets hurt or sick because of work and the employer is not insured, the employer is responsible for paying all the bills related to the injury or illness.

How is workers’ compensation premium calculated?

Payroll x Classification Rate x Experience Modifier = Premium

Workers’ compensation premium is based on the estimated amount of payroll paid to employees during the 12-month policy period. Employers can make a single payment or in a monthly installment.

After the 12-month policy has lapsed, insurance companies will require employers to check the actual payrolls that were paid to employees, which could result in additional premiums being due or a decrease in premiums at the end.

Do I need to post a Labor Law Poster?

The poster must state the name of the current workers’ compensation insurance carrier, the policy number and contact information. Employers also have to put the information of the workers’ compensation network next to the Labor Law Poster.

How do I get the Labor Law Poster?

Auto Insurance FAQs

Am I covered under my personal policy if I also use my auto for business?

If in addition to commuting to work, you also use your vehicle for other business-related driving, such as traveling on sales calls or carrying tools, supplies, and equipment to a job site, this is considered business use. It may or may not be covered under your personal policy.

To ensure that you have the appropriate insurance for your needs, consult with a qualified insurance representative and check your policy for restrictions.

If I borrow someone else's car, what insurance pays?

Can I convert my policy from term to permanent?

Do I need comprehensive and/or collision on all my autos?

After an accident, how do I file a claim against the other driver?

Does my auto insurance policy cover rental vehicles?

How can I save money on auto insurance?

- Increase your deductible

- Maintain a good driving record

- Maintain a good credit rating

- Take a driver safety course

Research before buying. Learn which cars are the least expensive to insure. KCAL Insurance offers discounts for cars that have anti-theft devices, air bags, and anti-lock brakes, for example. KCAL Insurance can give you free, no-obligation quotes on any cars you’re considering purchasing; just call us with the VINs of the vehicles you’re interested in buying. Take advantage of KCAL Insurance’s multi-policy discounts, which provide discounts on certain coverage when you purchase two or more policies, such as an auto and homeowners policy.

How much auto insurance do I need?

- How high should my liability coverage limits be? No one can predict exactly how much you would have to pay if you were to cause an accident. Ask yourself how you would pay for any damages exceeding your coverage limits. The higher your liability coverage limits are, the more likely your policy will be able to pay all of the damages.

- How high or low should my collision and comprehensive deductibles be? Higher deductibles lower your premium but increase the amount you must pay out of your own pocket if a loss occurs. Ask yourself how much you would be willing and able to pay on short notice in order to save on your premium.

- Should I carry collision and comprehensive coverage?

You may be required to carry collision or comprehensive coverage if your vehicle is leased or financed. Once you have paid off your car, and its value decreases, you might consider dropping this coverage to save money on premiums. However, consider whether the savings would be enough to offset the risk of having to pay the entire cost of repairing or replacing the vehicle.

How much liability coverage do I need?

If I loan my car, would I be covered if there's an accident?

Should I buy extra insurance protection on a rental car?

What discounts are available for auto insurance?

- Good Student Discount

- Mature Driver Discount

- Driver Training Discount

- Occupation Discount

- Special license and degrees

For more discounts, please check with your agent. Please drive carefully. To avoid accidents, don’t multitask in the car. Obey traffic regulations and go to traffic school to waive tickets when possible – your wallet will thank you for driving safely.

What happens if I'm a passenger in a friend's car and I'm injured as a result of an uninsured motorist?

What is a deductible?

What is not covered under my auto policy?

What is the difference between collision and comprehensive coverage?

- Your auto is struck by debris that falls from an overpass

- Your auto is damaged by a tree falling on it

- Your auto is partly or totally submerged in water

- Your auto is maliciously scratched

- Your auto’s tires are slashed

- Your auto’s windshield is cracked by a stone

Collision coverage pays for physical damage if your auto is hit by another vehicle or runs into an object. This coverage will pay for damage to your auto regardless of who causes the accident. Some examples of a collision loss include:

- Your auto strikes or is struck by another auto

- You hit a pedestrian, damaging your auto (the pedestrian’s injuries are covered under liability coverage)

- Your auto hits debris lying in the road

- Your auto strikes a tree or fence

- Your auto is struck by a shopping cart

What is Underinsured Motorists (UIM) coverage?

Who are covered drivers under my auto insurance policy?

Why do I need Uninsured Motorists (UM) coverage?

Will higher deductibles lower my auto insurance premium?

Will my insurance rates go up if I make a claim?

- Determination of fault

- Amount of damages paid

- State regulations

- Previous accident and violation (conviction) history

- Type of accident or violation

- Severity of accident or violation

Homeowners Insurance FAQs

I own antiques and fine art. What kind of coverage would adequately protect them?

If I have a loss, do I need to show proof of what was in my home?

What's Condo / Townhouse Insurance Policy?

What's Dwelling Fire Insurance Policy?

What's Homeowners Insurance Policy?

What's Renters Insurance Policy?

Medicare FAQs

What is Medicare?

Medicare is the medical health plan designed by the US government for individuals who are 65 or older. Certain younger individuals with disabilities or End-Stage Disease may also qualify for Medicare. This plan can help pay for partial medical costs, but does not include full coverage or most long-term care costs.

Who is qualified for Medicare?

- People who are 65 or older,

- People who are younger than 65 but have received disability benefits for over 2 years due to any disability,

- People with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant, sometimes called ESRD) or Amyotrophic Lateral Sclerosis (ALS).

What are the four different parts of Medicare? What is the difference between Medicare Parts A, B, C, and D?

Medicare Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

Medicare Part C (Medicare Advantage Plans): Offered by a private company that contracts Medicare to provide you with all your Part A and Part B benefits. Medicare Advantage Plans include Health Maintenance Organizations, Preferred Provider Organizations, Private Fee-for-Service Plans, Special Needs Plans, and Medicare Medical Savings Account Plans. If you’re enrolled in a Medicare Advantage Plan, Medicare services are covered through the plan and aren’t paid for under Original Medicare. Most Medicare Advantage Plans offer prescription drug coverage.

Medicare Part D (Prescription Drug Coverage): Part D adds prescription drug coverage to Original Medicare, some Medicare Cost Plans, some Medicare Private-Fee-for-Service Plans, and Medicare Medical Savings Account Plans. These plans are offered by insurance companies and other private companies approved by Medicare. Medicare Advantage Plans may also offer prescription drug coverage that follows the same rules as Medicare Prescription Drug Plans.

When you apply for Medicare at the Social Security Office, after joining Part A and Part B, you still need to purchase Part C and Part D through an insurance agency. You need to make sure you have Prescription Drug Coverage in order to avoid the liability for a lifetime penalty or the cost generated from prescription drug purchase, which will increase your economic burden.

What is Medicare Advantage (Part C)?

Part C also provides coverage for prescription drug purchases, which is also covered under Part D. Besides all the benefits mentioned above, Medicare Advantage also provides benefits for vision, dental, acupuncture, hearing aid and medical transportation, which are not covered under any other plans.

Part C can be categorized into two types: PPO and HMO

PPO: Medical cost will be taken care of by the insurance company and original Medicare. You can choose any in-network doctors for services and it provides coverage through 50 states.

HMO: The insurance company and independent practice association (IPA) have shared responsibility for your medical cost. The insurance company will pay for high cost services such as hospitalization and emergency care while IPA will pay for low cost services such as preventive care. You will need a referral from the assigned primary care physician (PCP) before you can see any other health care professionals, which has to be within 30 miles of your residence.

Part A and B only cover 80% of the medical cost, how I can get the rest covered?

Medicare Supplement provides coverage for the out-of-pocket amount not covered in Part A and Part B. Part D provides coverage for costs generated from prescription drug purchases.

Option Two: Purchase Medicare Advantage (Part C)

Medicare Advantage not only provides coverage for the out-of-pocket amount not covered in Part A and Part B, but it also covers the cost generated from prescription drug purchases. Meanwhile, it also provides other medical benefits.

How much does Medicare cost?

Hospital Insurance (Medicare Part A): If you live in the US for more than 10 years, and have paid federal Medicare tax when you were working, then you will receive free Part A coverage; if you are already 65 years old, but haven’t worked over 10 years, you have to pay a monthly premium for Part A up to $499 per month (in 2023).

Medical Insurance (Medicare Part B): In 2023, the monthly standard premium for Part B is $164.90. However, if your retirement income is over $97,000 for a single person or $194,000 for a retired couple, you have to pay a higher monthly premium for Part B as the standard request. One thing you need to pay attention to is if you don’t apply for Medicare Part B during the Initial Enrollment Period, you may need to pay higher Part B premium for joining later.

Medicare Advantage (Part C): The premium depends on which plan you enroll in.

Prescription Drug Coverage (Part D): The premium depends on which plan you enroll in.

When can I apply for Medicare?

If you are eligible for Medicare because you are 65 years old, the Initial Enrollment Period begins three months before you turn 65, including the month of your 65th birthday, and ends three months later.

Whether you are retired or already starting to receive Social Security, you need to contact the Social Security Office three months before turning 65 years old to apply for Medicare.

What is the result for not applying for Medicare on time?

If you don’t apply for Medicare Part B during the Initial Enrollment Period, you can still apply between January 1st and March 31st each year. The policy will be effective on the first day of the following month. However, for each 12-month period delay, your monthly premium for Part B will increase by 10%.

Besides that, you need to purchase Part C and Part D through your insurance agency. Without Prescription Drug Coverage (Part D), you will be liable for a lifetime penalty and the costs generated from prescription drug purchases will increase your economic burden.

If my employer has provided me with group health insurance, do I still need to join Medicare?

Where can I apply for Medicare?

Social Security Office: 800-772-1213 Mon – Fri, 8AM – 7PM

https://secure.ssa.gov/ICON/main.jsp

Office Hours:

| Monday | 9AM – 3PM |

| Tuesday | 9AM – 3PM |

| Wednesday | 9AM – 12 Noon |

| Thursday | 9AM – 3PM |

| Friday | 9AM – 3PM |

Business Insurance FAQs

What are my coverage options?

What are the benefits of Business Owners Insurance?

- Damage or destruction to your business vehicles

- Certain liability exposures resulting from the operation of your business vehicles

- Damage or destruction to your office equipment or inventory

- Loss of income in case you have to suspend your business temporarily due to a covered loss

- Certain business related liability exposures such as wrongful entry or search, libel, slander, and even certain offenses arising out of your business’s advertising

- Risks to your cargo while in transit or storage

- Theft or loss of tools and equipment

- Crime coverage including robbery, burglary, even employee dishonesty

What are the benefits of Commercial Auto Insurance?

- Liability Coverage: In case you’re sued as a result of an auto accident.

- Collision Coverage: Helps cover physical damage to your vehicle due to collision or upset.

- Comprehensive Coverage: Helps cover physical damage to your vehicle due to fire, theft and glass breakage.

- Rental Reimbursement Coverage: Helps cover the cost of a replacement vehicle for a specified period of time when your vehicle is disabled due to an insured loss.

What is Business Liability/Commercial General Liability Insurance?

Your business is exposed to liabilities every day. The only way to protect your assets is to carry adequate business liability insurance. A Commercial General Liability (CGL) insurance policy is the first line of defense against many common claims.

General Liability insurance covers claims of bodily injury or other physical injury or property damage. It is frequently offered in a package with Property insurance to protect your business against incidents that may occur on your premises or at other covered locations where you normally conduct business. Commercial General Liability enables your business to continue operations while it faces real or fraudulent claims of certain types of negligence or wrongdoing.

Travel Insurance FAQs

If I want to go back to China to treat a pre-existing condition, will the insurance company provide coverage for my medical costs?

What is the minimum number of days of coverage for Foreign Student Insurance?

If I need to travel to more than one country, do I need to submit an application for each country I go?

No. You only need to submit once. When filling out the application form, please use the first country you arrive as your destination country.

Do I have to wait until I arrive in the USA and then go to KCAL’s office to fill out the application for travel insurance?

Does travel insurance provide coverage for onset of chronic disease during the trip?

Do I have to pay anything else besides the daily premium?

How long will it take for my travel insurance to become effective?

If I am a Green Card holder or have dual citizenship, and I want to travel back to my country of citizenship, how should I purchase travel insurance?

Travel insurance cannot be purchased by those returning to their country of origin/hold citizenship in that country.

If I would like to change the insurance content, such as name, birthdate, or a change in travel plans, how do I cancel the travel insurance?

You can be refunded up until the insurance expires, but the insurance company will charge $25 for a processing fee, and only the unused portion will be refunded. Only the insured who has not filed a claim can get the partial refund. If you want to change or cancel something, it must be written out and forwarded via mail, fax, or email to the Travel Insurance Customer Service Center.When sending correspondence, please include a daytime phone number and reference your Online Order Transaction number.

• Visit-USA: info@travelinsure.com,or mail to Travel Insurance Services (3805 West Chester Pike, Suite 200 Newtown Square, PA 19073, USA), or fax to 610-537-9825.

• InterMedical: imed@travelinsure.com or mail to Travel Insurance Services (3805 West Chester Pike, Suite 200 Newtown Square, PA 19073, USA),or fax to 610-537-9818.

• WorldMed: worldmed@travelinsure.com or mail to Travel Insurance Services (3805 West Chester Pike, Suite 200 Newtown Square, PA 19073, USA),or fax to 610-537-9831.

Do my family and I need to purchase separate insurances?

The primary insurer and the family will only need to purchase one. Please fill in the Spouse column for the spouse, and children under Dependent. Everyone’s coverage and plan will be the same.

I want to extend the effective date of my travel insurance, what should I do?

You can buy the same insurance again (that is, buying a new insurance). For your new insurance, please fill in the next day of your current insurance’s expiration date. Please note that the fastest effective date for travel insurance is the day after you submitted the application.

What is a beneficiary?

The beneficiary is the individual that receives the insurance benefits. The principal insurer can fill in anyone other than themselves as the beneficiary. If the principal insurer dies due to an accident or sudden illness, the beneficiary can receive the compensation. There can only be on beneficiary.

What is the Additional AD&D?

Additional accidental death and disability benefits: death, loss of limbs or sight will be paid to you as specified in the attached schedule amount.

If an incident of loss occurs and it is caused or contributed by the following situations, you will not be within the insurance coverage:

- A terrorist attack, war or an act or war, whether declared or undeclared

- Your participation in insurrection, rebellion, or riots

- You are serving in the armed forces of any country

- Suicide or attempted suicide or self-harm, whether you are deemed sane or insane

- Voluntary use of any chemical compound, poison, or drug, unless you are directed by a licensed physician

- Committing or attempting to commit a felony

- Illness, mental illness, or pregnancy

- The accident was caused by intoxication as defined by the law’s jurisdiction, whether directly or indirectly

- Myocardial infarction or cerebrovascular accident (CVAV/stroke)

- Infections, except wound infections caused solely by accidents

- If you are injured while flying an aircraft, learning to fly an aircraft, serving as an aircraft crew member, or if the aircraft is being used for any purpose other than passenger transportation, including traveling on, boarding, and disembarking

- Medical or surgical treatment of any of the above

- Any non-insurance covered physical activity

What kinds of recreational sports are covered with insurance?

General recreational sports played during your visit to the United States are covered by travel insurance. If it is a sport that requires wearing safety equipment or a life jacket, the insurance company will only cover it if you wear it. The following sports are not covered by general travel insurance for visiting the US:

• Big Game Hunting or Safari

• Bungee Jumping, Hang-Gliding, Kitesurfing

• Mountaineering (at elevations below 4,500 meters)

• Parachuting, Paragliding

• Powerlifting

• Running with the Bulls

• Sky Surfing

• Recreational Downhill and/or Cross-Country Snow Skiing and Snowboarding (no cover provided while skiing away from prepared and marked in-bound territories and/or against the advice of the local ski school or local authoritative body)

• Spelunking

• Sub Aqua Pursuits involving underwater breathing apparatus (accompanied by a certified instructor at depths less than 10 meters, or PADI/NAUI certified)

• Surfing, Waterskiing, Whitewater Rafting

What are Intercollegiate Sports Coverage?

Intercollegiate sports refer to team or competitive sports played at the college level. If you want to be covered, you must check the box, such as football, soccer, and baseball.

What are Hazardous Activities?

Adventurous activities: those who are insured and plan to participate in adventurous activities during international travel can purchase this add on for an additional 20% of the premium. This benefit covers the medical expenses only. To participate in the following types of activities, you need to check the box for the item, or else it will not be covered.

• Big Game Hunting or Safari

• Bungee Jumping, Hang-Gliding, Kitesurfing

• Mountaineering (at elevations below 4,500 meters)

• Parachuting, Paragliding

• Powerlifting

• Running with the Bulls

• Sky Surfing

• Recreational Downhill and/or Cross-Country Snow Skiing and Snowboarding (no cover provided while skiing away from prepared and marked in-bound territories and/or against the advice of the local ski school or local authoritative body)

• Spelunking

• Sub Aqua Pursuits involving underwater breathing apparatus (accompanied by a certified instructor at depths less than 10 meters, or PADI/NAUI certified)

• Surfing, Waterskiing, Whitewater Rafting

What is Crisis Response?

Crisis response covers kidnapping, ransom, natural disaster evacuation and other costs related to crisis response. Each person enrolled needs to pay an additional $1.40 per day.

Life Insurance FAQs

Can I renew my term life policy after the initial term expires?

How can I save money when buying life insurance?

If you want Permanent Life but you’re on a budget, consider some Term for now. You can save money initially by buying some Term Life in combination with Permanent Life. Later on, if your budget increases, consider converting the Term policy to Permanent Life. Consider group life insurance offered through your employer. It may be available at a low cost. But keep in mind that your group coverage may end or become more expensive when you leave your job.

How do I know what term to select?

How much insurance do I need?

How much will life insurance cost me?

The type of policy you purchase will also affect the amount of the premium. Rates for term insurance are typically lower, at least at younger ages. Premium rates for permanent policies like Whole Life are typically higher at earlier ages, but do not increase as you age. Lastly, paying premiums monthly or quarterly rather than annually will result in higher premiums.

In addition to protection, what am I trying to accomplish with my life insurance?

What are some of the reasons for converting to a permanent life insurance policy?

What are the tax advantages of life insurance?

Pursuant to IRS Circular 230: The information contained in this website is not intended to (and cannot) be used by anyone to avoid IRS penalties. This website supports the promotion and marketing of insurance products. You should seek advice based on your particular circumstances from an independent tax advisor.

What if I already have insurance coverage?

- Were recently married or divorced

- Have a child or grandchild who was recently born or adopted

- Provide care or financial help to a child or parent

- Want to ensure that financial resources are available to provide assistance or long-term care for a loved one

- Purchased a new home recently

- Have children or grandchildren who are about to enter college

- Refinanced your home mortgage in the past six months

- Receive an inheritance

- Retired or your spouse has retired

- Have started a business